“Just a guy from the islands…”

My background is in physics and math: I’m passionate about the role of solid, comprehensive research, and I want to understand the network-structure behind the dynamics we observe in the world. In financial markets, the value there is strongly underestimated in managing market, credit and liquidity risk, imho. Beyond that I’m always in for interesting cross-disciplinary research, always looking for new insights and novel takes on the world.

You’ve found my research and project portfolio: nothing here should in any way be construed to represent the views of my employer, or investment advice in any sense of the term.

I currently do cross-asset strategy, based on quantitative modeling of financial markets. I’ve concurrently run global equity portfolios, and before that did design and implementation of predictive-analytics systems for asset management, and occasional (market-risk and alpha-) model validation. In larger projects I’ve typically run a small team of specialists as technical lead.

I hail from a tiny island called St. Martin in the Caribbean, and love languages in the broad sense. I speak:

- English and Dutch natively,

- French and some Spanish and Portuguese,

- and of course math & code …

Applied & Data Science :: Recent

-

Holmes (2014 – )

Work on a novel general inference engine (i.e. an AI in the full-blown AGI sense) which recognizes patterns in (multiple) sensory data (streams) over time. The engine predicts and influences its environment to increase the likelihood of the occurrence of the goals driving its motivation. Design leverages Cassandra on GCP, Python and SQL; with a guy called Molanus.

-

Active Bet-Sizing (2018)

Designing a custom approach to combining (fundamental) conviction with (systematic) risk-balanced portfolio-construction in a hybrid fundamental/quant approach. Tailored models, implementation tools and visualization delivered with Matlab & Python.

-

Quant Equity Alpha Models (2017-2018)

Tying together stock-level and aggregated (e.g. sector or region) quantitative signals for bottom-up and top-down market views, to an optimization- and backtesting-framework for studying portfolio construction decisions. Bridges the Kelly-perspective and cross-sectional regression approaches. Matlab development integrated with multiple production datafeeds.

Applied & Data Science :: Older

-

Analytics & Architecture (2013-2018)

- Portfolio Management Platform Redesign: Ran a major upgrade and harmonization of the full tooling and workflow setup for cross-asset portfolio management covering teams in 3 countries: data flows and precedence hierarchy, screens, optimization engine, trades, performance and risk analysis and production reporting, plus user training.

- “Analytical Environment” Product Owner (team of 10): Delivered architecture for a core regulatory-compliance system across the firmwide product-offering to retail and private clients; design was dual-purposed as analytics environment to enable extraction of value through data-science & analytics in the business; SAS-based.

- “Pandora” Analytics Team-Lead (team of 4): Developed a full investment performance and risk analytics system, with the goals of speedy, daily reporting and data provision to portfolio management teams. SAS development integrated with Factset, the FIS APT risk-engine, in-house datafeeds on a historicized DataVault design.

- SAS MI Team-Lead (team of 5): Developed an analytics (BI/MI) platform for client holdings and asset flows over time. Architecture, ETL, DataVault approach to DWH, custom reporting engine, end-to-end flows, performance testing. SAS development, integrated with custom reporting engine.

- Enhanced Reporting Framework Team-Lead (team of 2): Developed a unified framework for efficient, clean and modern reporting elements and style, designed for modular integration with data-warehousing and quantitative analytics solutions; SAS development.

-

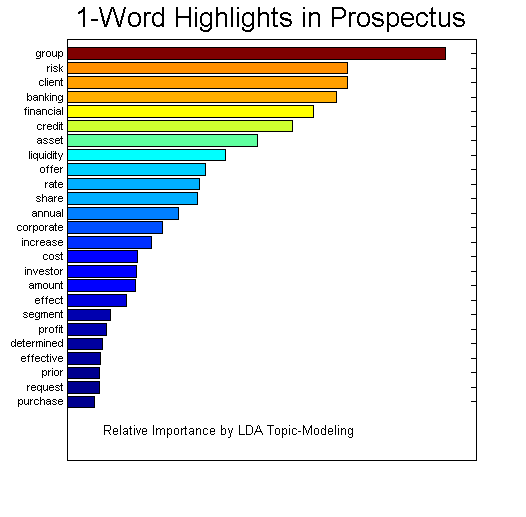

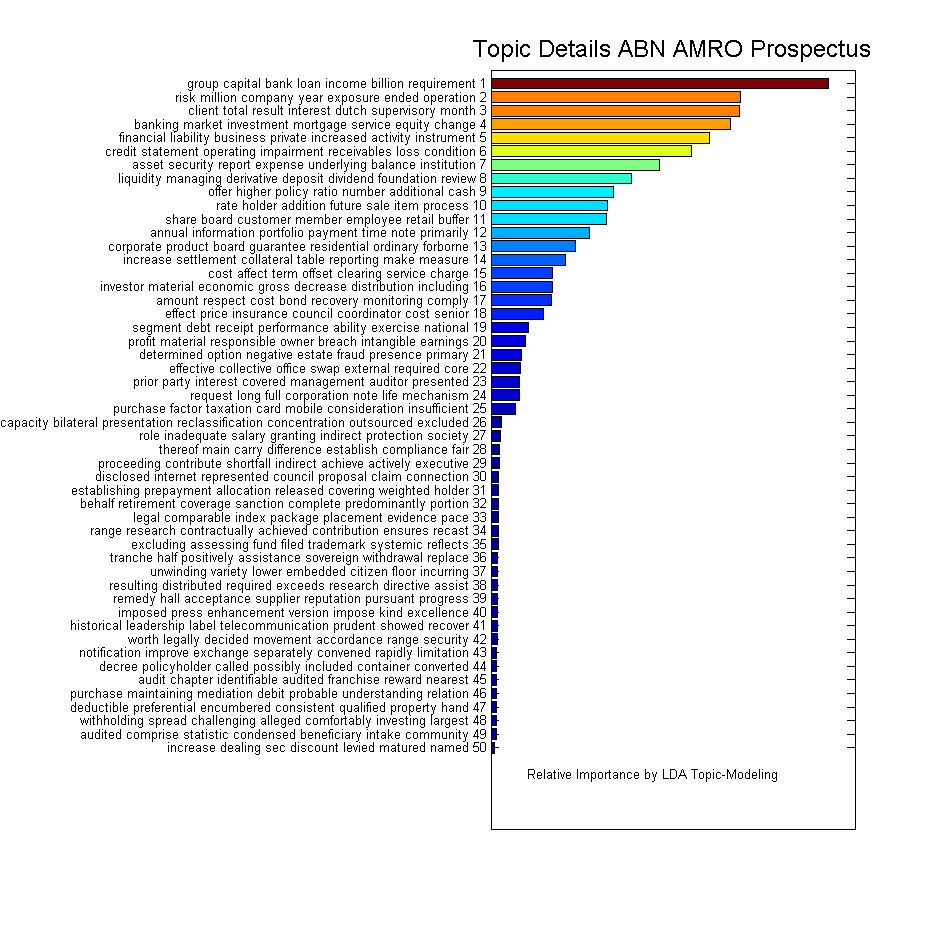

NLP on the ABN AMRO prospectus (2015)

Combining techniques from probabilistic topic modeling (using LDA) with simple visualization techniques to identify clusters of topics discussed in the prospectus of my employer when they IPO’d back in late 2015. This refurbished some of the code from the Pensamiento paper, but the neat results are just the visuals: summarizing an entire prospectus’ key topics in a one-word-summary, and by topic. For more details, check out the Python at [github]

-

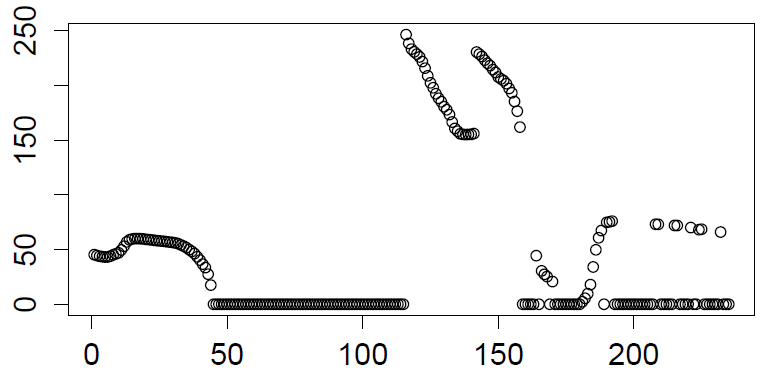

LPPL Financial Crashes (2014)

Implemented a predictive model of financial crashes driven by herding behavior, which is expressed through log-periodic power-law oscillations. Based on the research of Didier Sornette, SSRN. A nice visualization to understand these somewhat unstable models (implemented naively) is to ask the question “how do we know the prediction is stable”, as encouragingly indicated by the plateau at about t=+50 days (y-axis, forward in time) from t=0 (x-axis, backward in time) in this figure. Older example code on github, unfortunately broken by the now-defunct yahoo-finance interface.

-

“Investment Game” for Charity (2014)

Developed the models for, and major parts of a full transaction-processing, analytics and reporting stack for an “Investment Game” organized for the benefit of the Children’s Khazana Foundation, running live during the 2014 World Cup, as a complete and investable securities market; a preprint describing the modeling is on SSRN. Matlab models, SAS implementation in production.

-

Exchange Matching Engine (2011)

QuantCup 2011 competition entry, implementing an exchange matching algorithm. Ugly C++ code on github.

{kind=link}

{kind=link}

{kind=link}

-

NEGF in ADF/BAND (2008-2012)

Developed a scalable, high-performance, quantum-chemical NEGF transport code (Physics PhD), which was later integrated into a commercial quantum-chemistry modeling solution. Developed a scalable, high-performance, quantum-chemical NEGF transport code, which was later integrated into a commercial quantum-chemistry modeling solution (SCM’s ADF/Band package). Fortran multicore supercomputer-ready code, Python postprocessing.

-

GSM-R for NCBG (2010)

Designed a statistical methodology for validation of GSM-R networks during field-trials on the high-speed railway networks in the Netherlands and Belgium, later used in the design of a network in Tunisia. Developed software for transmission interference analysis and cell-tower lookups (consulting as Radio Network Planner for ClearCinCom). Perl and VB development.

Academic Projects

-

An Investment Game (2017)

Derived from a real event run for charity during the 2014 World Cup on the basis of the models introduced here, this presents a novel investment game, taking a quantitative finance approach to football tournaments. Published in Wilmott, SSRN. Matlab models.

-

Ebola Outbreak Spread Models (2016)

Derived from work at a summerschool at the Santa Fe Institute, developed models describing the essential dynamics of the 2014-2015 Ebola outbreak in West Africa. We focused on understanding the qualitative dynamics of SIR-class models, and how deviations correlated spatially and temporally with observed real-world features like border closures, geospatial migration networks, and genetic variation. Published in NatureSciRep, SSRN. Python development combining mathematical SIR models with NetworkX and geomapping.

-

Convergence in the Sciences (2015)

Based out of the Santa Fe Institute, developed an analysis of temporal trends in research, and distance-measures to quantify distance between clusters of research topics using only primary texts and LDA (latent Dirichlet allocation) based topic modeling. Published in Pensamiento, and in preparation for publication we put a preprint with some of the work here in the CSSS15 proceedings. Python/Matlab development, building on Mallet & NLTK.

Academic Vita

Post-Doc

- I did a short Postdoc to integrate my models into the commercially available ADF/Band quantum-chemistry code. I worked on this with van Gisbergen and Philipse at SCM, a spinoff of the Theoretical Chemistry group at the Free University (VU) in Amsterdam.

Doctorate

-

My Ph.D. research was on better models for electronic transport in single-molecule nanostructures, to understand molecular-electronics experiments at the Kavli Institute of Nanoscience in Delft. Work was on quantum transport and quantum chemistry, and required extensive HPC parallel algorithm design (run on the Huygens supercomputer @SARA). We:

- developed a code for single-molecule transport modeling, arXiv, JPhysChemC

- explained some neat experiments, arXiv, NatureNano

- and extended the theory a bit, arXiv, JChemPhys

- while establishing the feasibility of way cheaper methods you should probably use first. arXiv, JChemPhys

- used for some neat thermo-electricity calculations as well, arXiv, JChemPhys

Master’s

-

My M.Sc. built on work I started at CSR at the University of Texas in Austin, developing numerical algorithms aware of the dynamical structure in the equations governing satellite orbits, to provide more accurate simulation of trajectories from:

- an astrodynamics angle: Numerically-conservative integration in N-body problems

- an applied math angle: Approximations to 1st Integrals in N-body problems

- code [github]